library(tidyverse)

library(reglin)

set.seed(1234567890)

n <- 100

simdata <- data.frame(

x1 = rnorm(n),

x2 = rnorm(n),

x3 = exp(rnorm(n))

) |>

mutate(

y = simdata <- rlm(~ x1 + x2 + log(x3), beta = c(2.3, 0, 1.7, 1), sigma = 1)

)

glimpse(simdata)

#> Rows: 100

#> Columns: 4

#> $ x1 <dbl> 1.34592454, 0.99527131, 0.54622688, -1.91272392, 1.92128431, 1.3719…

#> $ x2 <dbl> -0.67596036, 1.50263254, 1.02472510, -0.38030432, 1.92037360, 0.276…

#> $ x3 <dbl> 0.6216812, 2.9560186, 1.1340223, 1.9540347, 1.0850314, 1.3069312, 0…

#> $ y <dbl> -0.40846685, 6.95514925, 4.85219640, 3.27567494, 5.42484220, 3.3157…

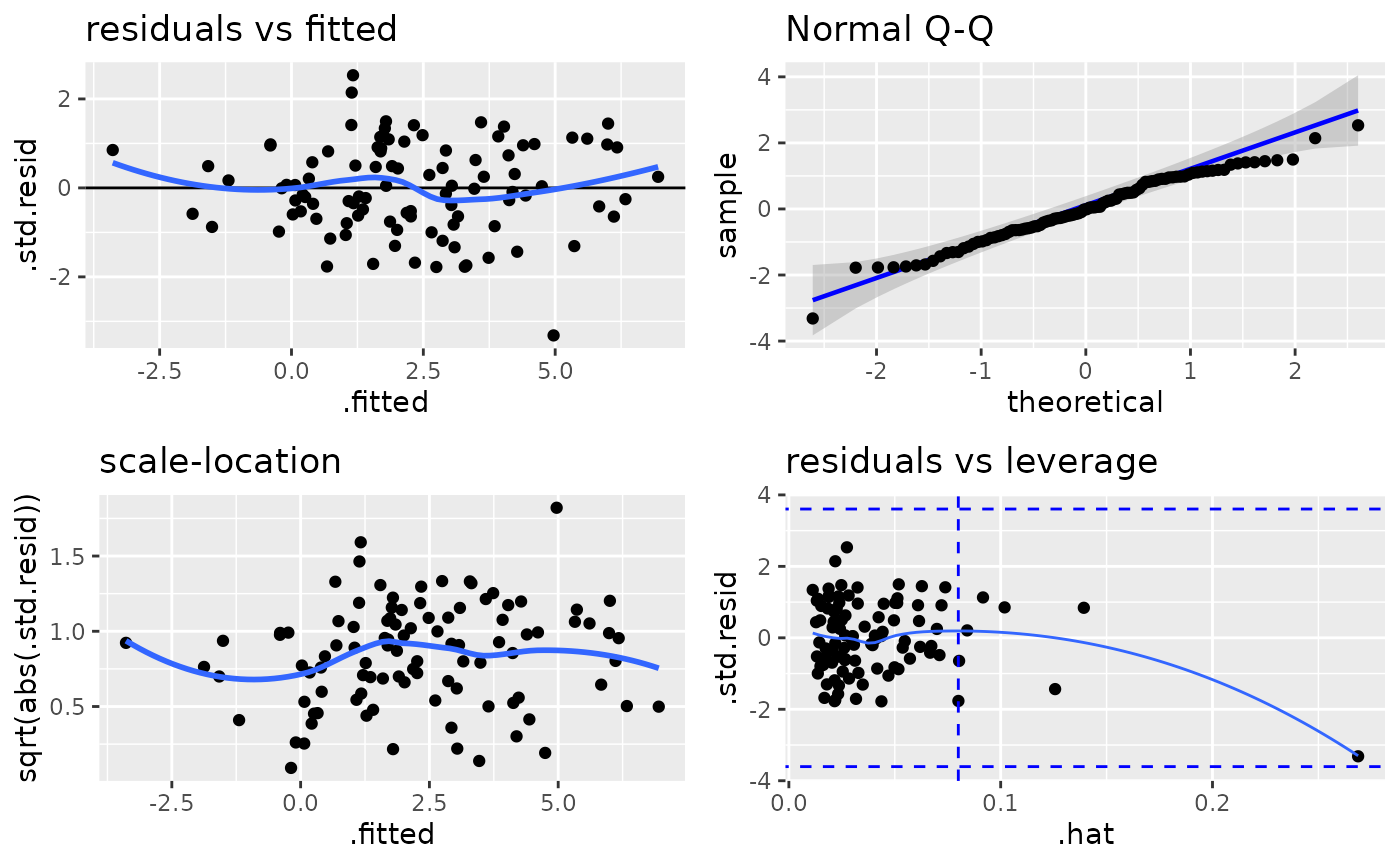

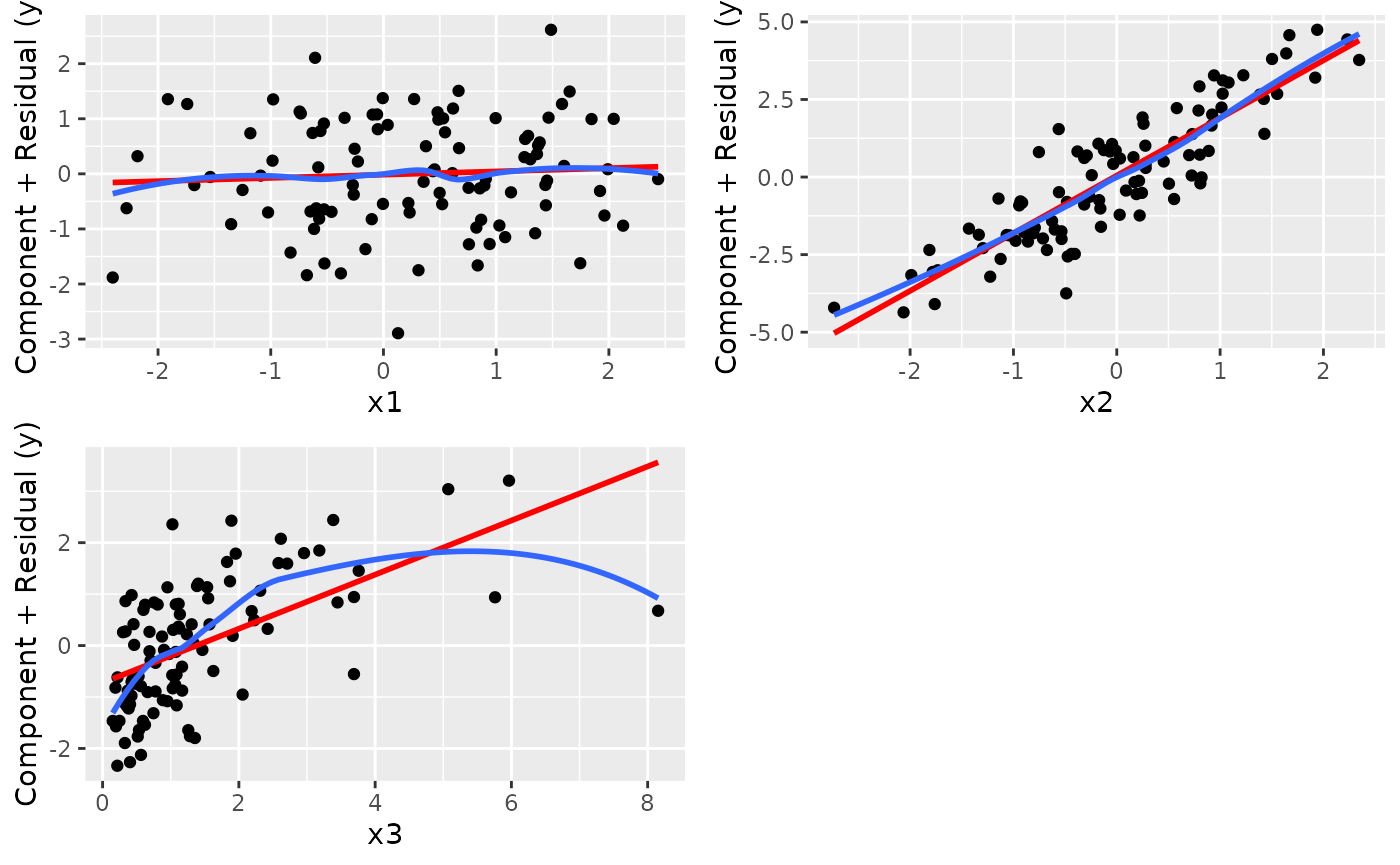

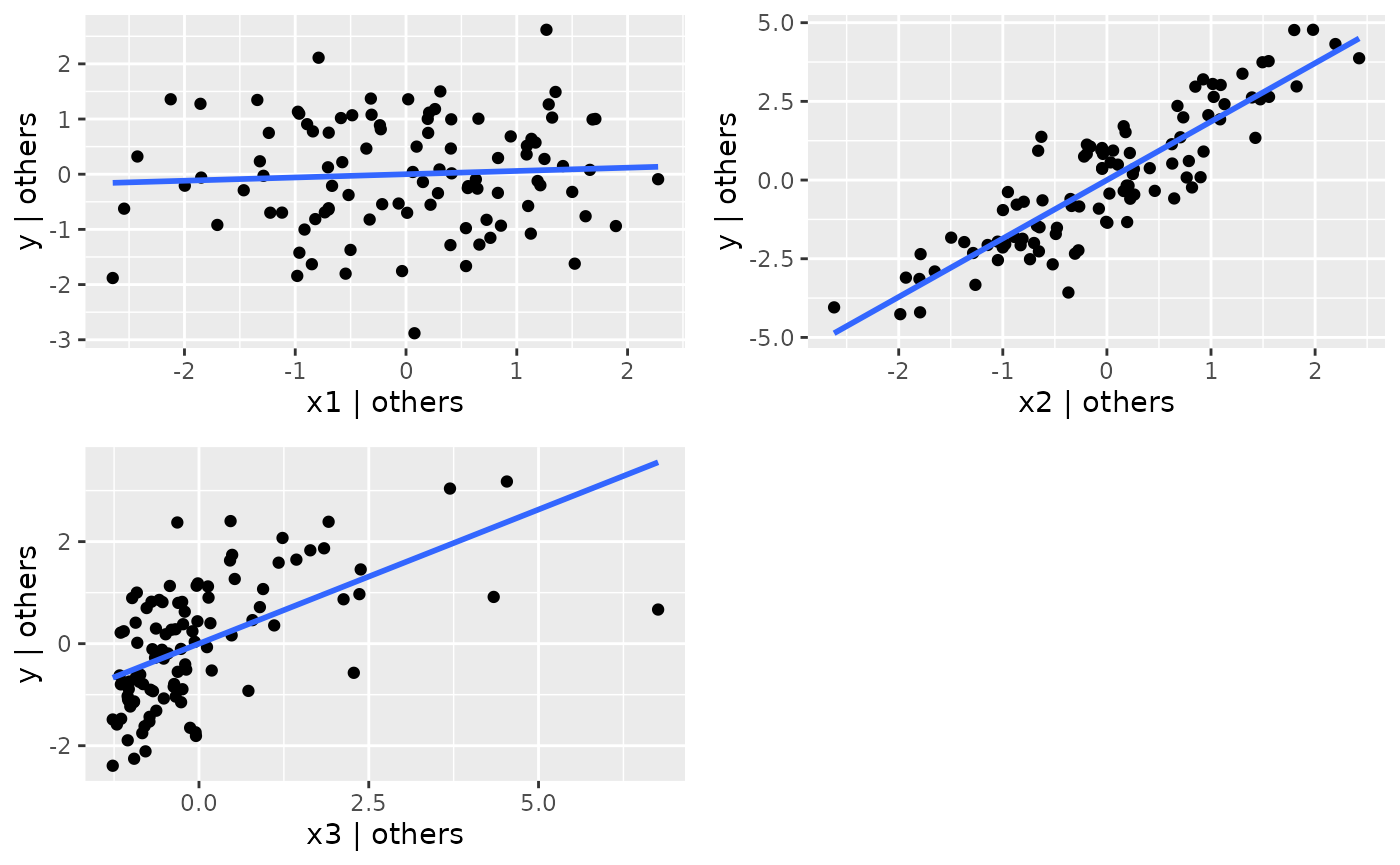

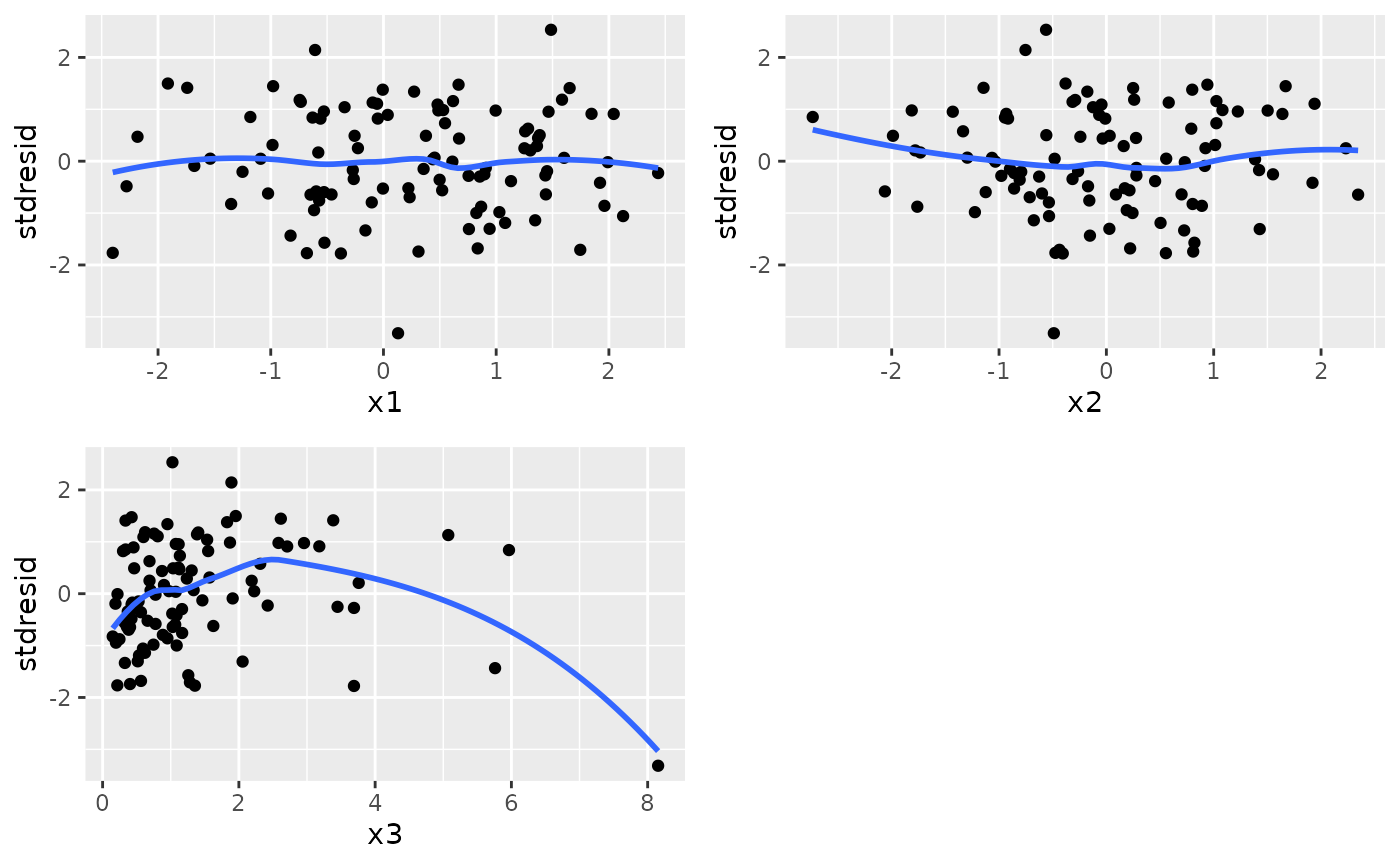

# escala incorreda de x3:

fit <- lm(y ~ x1 + x2 + x3, data = simdata)

ggresiduals(fit, type = "default")

# testes:

testResiduals(fit)

#>

#> Shapiro-Wilk normality test

#> W p.value

#> 0.987 0.4373

#> ------

#>

#> Non-constant Variance Score Test

#> Variance formula: ~ fitted.values

#> Chisquare = 1.397527, Df = 1, p = 0.23714

#> ------

#>

#> Durbin-Watson Test for Autocorrelated Errors

#> lag Autocorrelation D-W Statistic p-value

#> 1 -0.08969188 2.165836 0.412

#> Alternative hypothesis: rho != 0

#> ------

#>

#> Bonferroni Outlier Test

#> No Studentized residuals with Bonferroni p < 0.05

#> Largest |rstudent|:

#> rstudent unadjusted p-value Bonferroni p

#> 96 -3.50531 0.00069782 0.069782

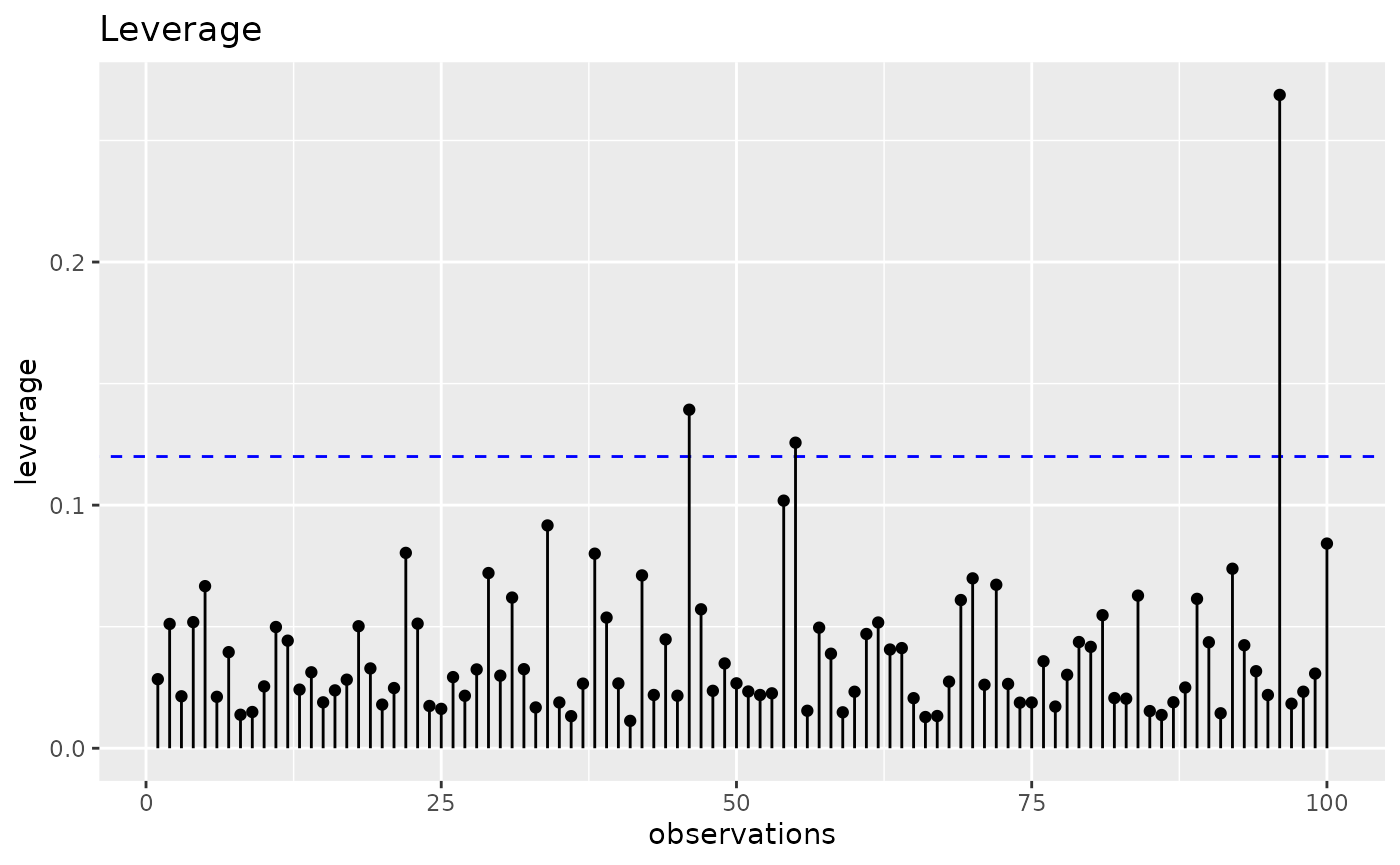

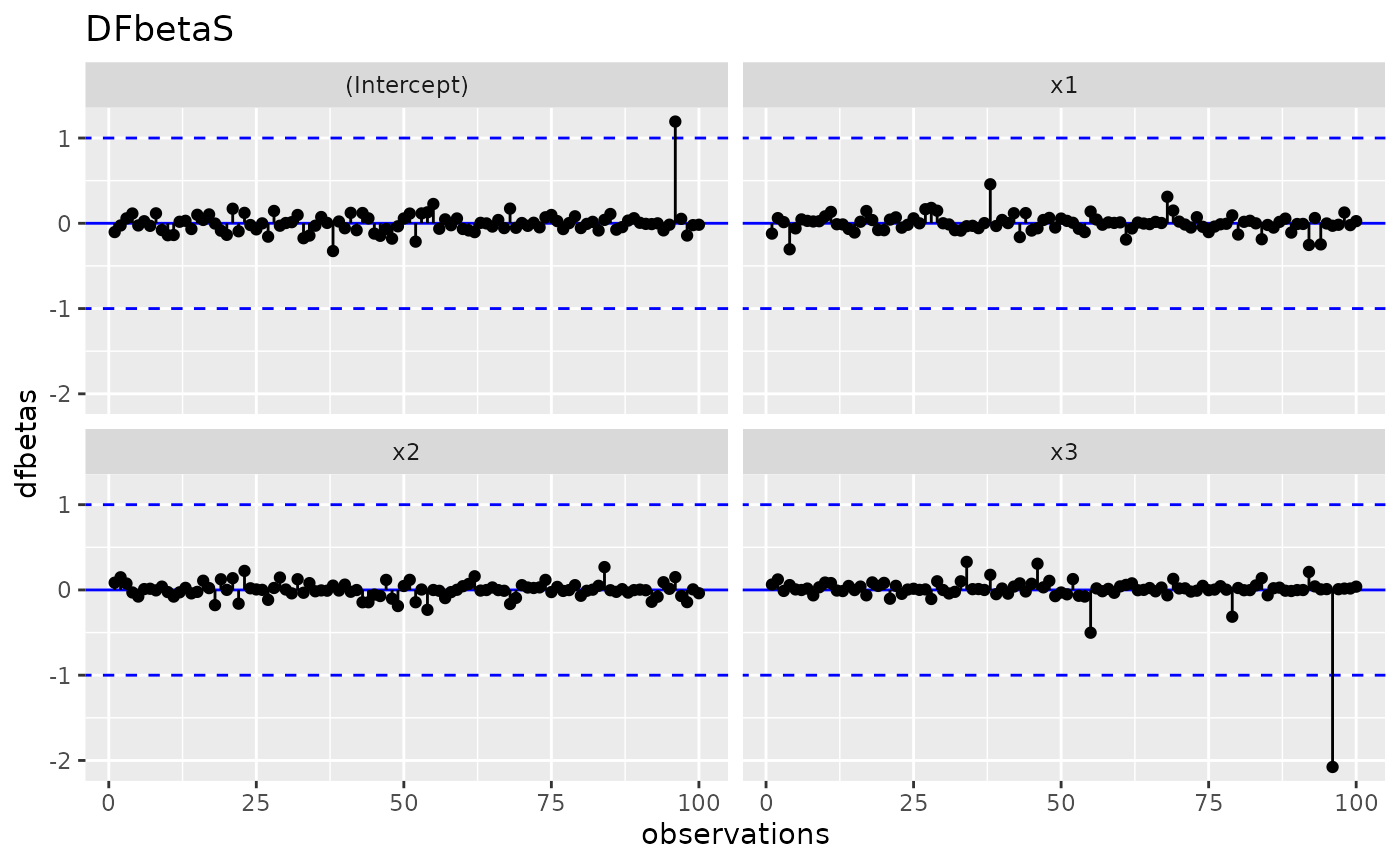

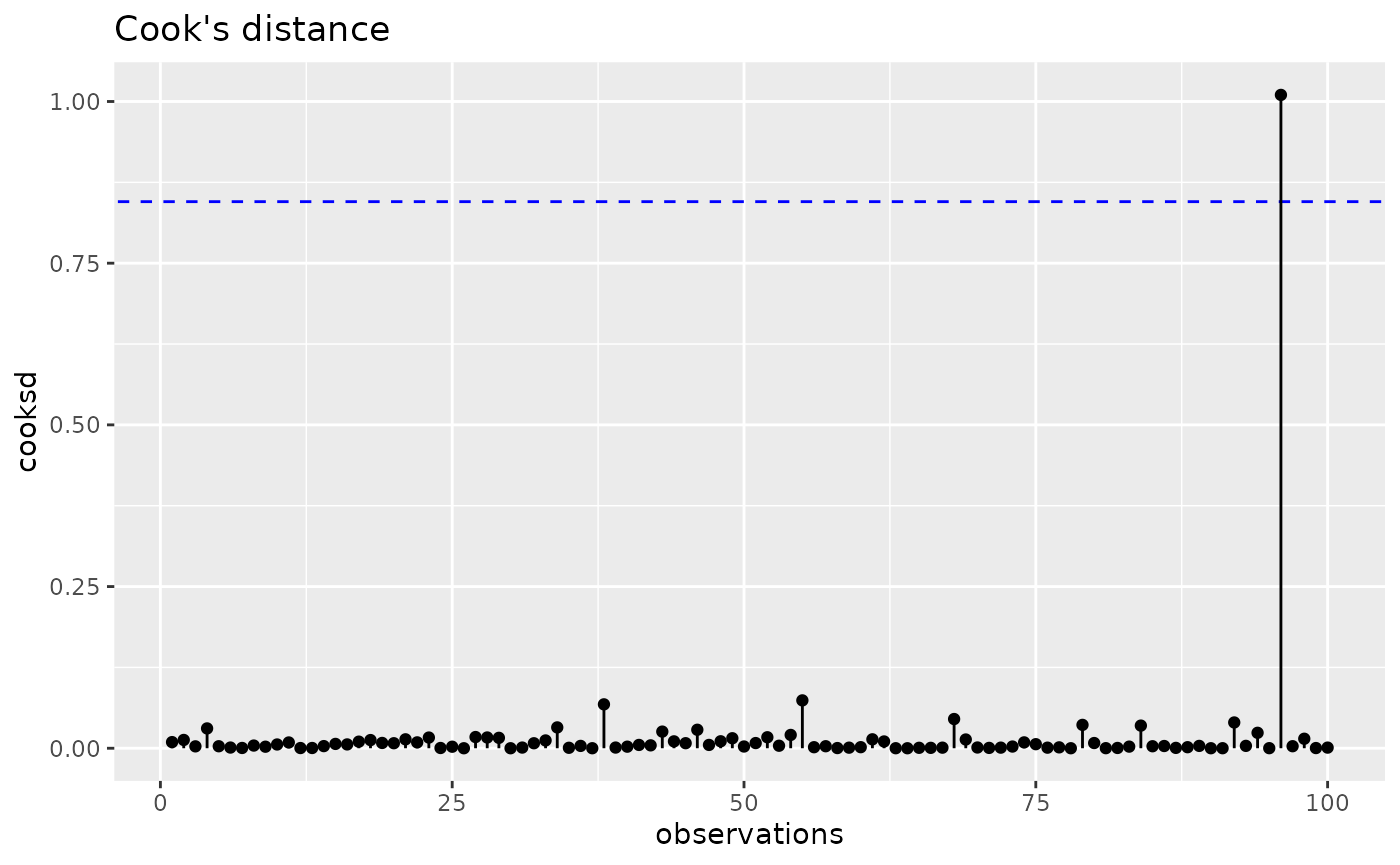

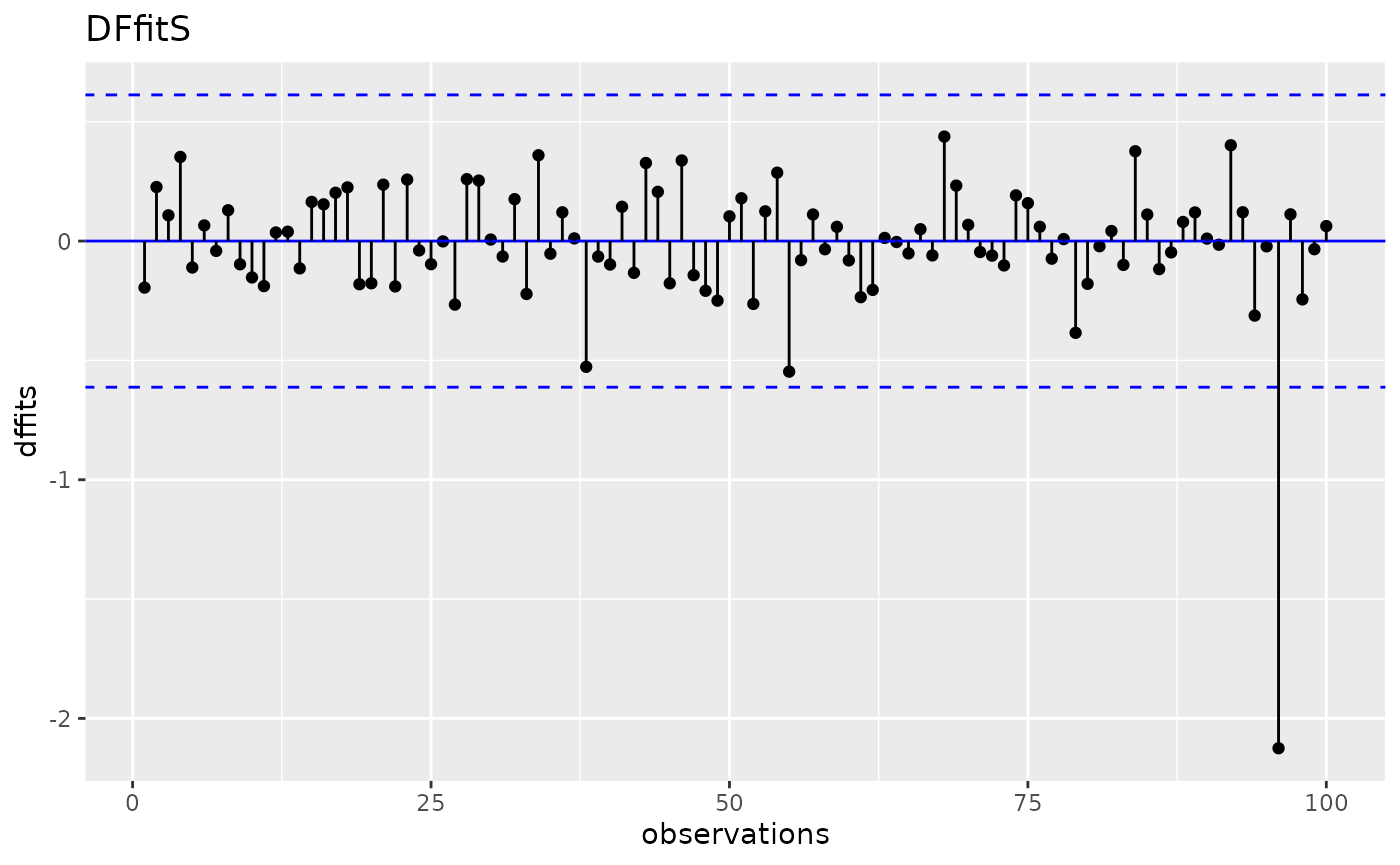

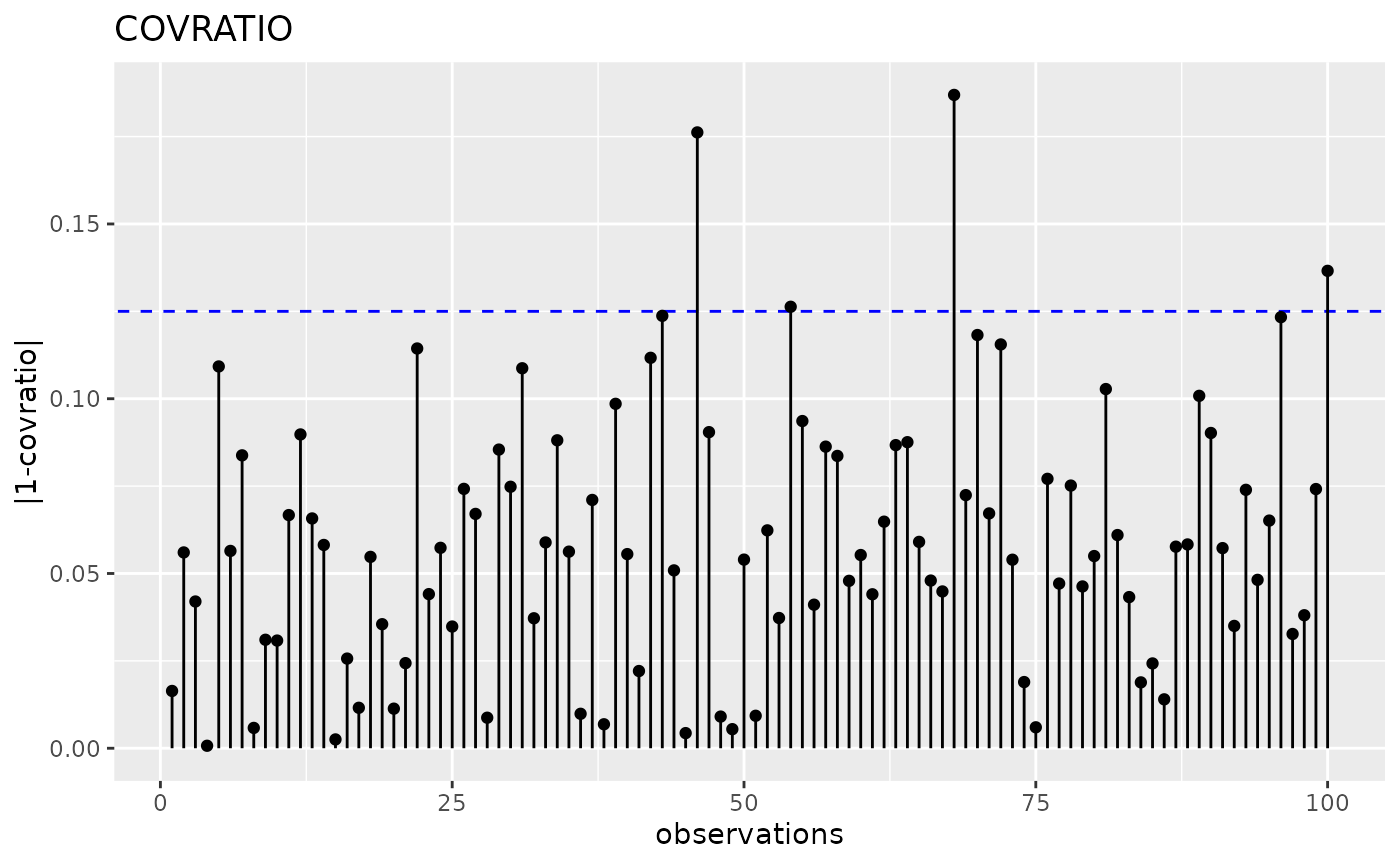

# análise (gráfica) de influência:

gginfluence(fit, measure = "leverage")